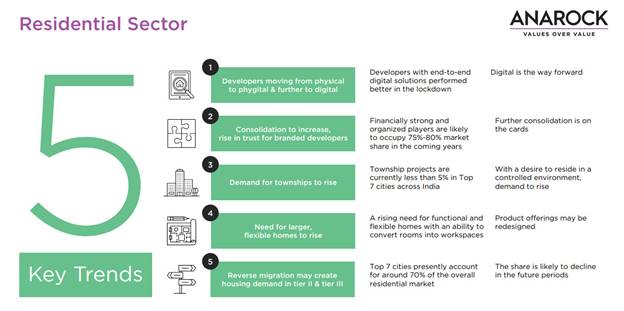

Indian real estate is bracing itself for a very new post-COVID-19 world. One significant trend may be reverse migration spurring housing demand in Tier 2 & 3 cities, says the ANAROCK report ‘India Real Estate: A Different World Post COVID-19’. Currently, the top 7 cities account for almost 70% of India’s residential market, with the remaining 30% accounted for in Tier 2 & 3 cities. This ratio may well change in times to come.

Cities like Lucknow, Indore, Chandigarh, Kochi, Coimbatore, Jaipur and Ahmedabad would be the main beneficiaries of the reverse migration of professionals who have lost their jobs in the metros, or are likely to. These returnees will benefit from the cost of living and superior infrastructure that many Tier 2 and Tier 3 provide.

Anuj Puri, Chairman – ANAROCK Property Consultants says, “Reverse migration is already very visible among migrant labourers, and this trend can further percolate to skilled professionals who have been or may be off-rostered. Smaller towns and cities would consequently see a spurt in housing demand. Primary demand may skew towards rental housing – purchase demand would initially come from local investors keen to meet the rental demand. Many NRIs will also return to India amidst dwindling job prospects, particularly in the US and European nations which account for nearly 70% global cases. For them, the top 7 cities would be the best options but many will consider smaller cities where they can be close to their families. Finding suitable employment for reverse-migrating Indians in smaller cities may prove to be challenging.”

- ANAROCK’s recent consumer survey taken during the lockdown period indicates that of the respondents who preferred to invest in Tier 2 & 3 cities in 2020, 61% are end-users and almost 55% are aged under 35 years. At least 47% of respondents are focused on affordable properties priced within INR 45 lakh, followed by 34% who are looking for mid-segment homes priced between INR 45-90 lakh.

- The residential segment will see a manifold increase in demand for townships projects which offer a controlled environment. In terms of supply, township projects have less than 5% overall share in the top 7 cities as on date.

- Further market consolidation is expected with the increased preference for branded developers. Financially strong organized players are likely to occupy 75%-80% market share in the coming years.

Office & Retail Real Estate

Commercial Real Estate – In office real estate, social distancing norms may increase the per capita office space allocations even as a segment of employees will work from home. During the last decade, per capita office space allocation reduced from 100-125 sq. ft. to 75-100 sq. ft. in the pre-COVID-19 period of January 2020.

Safety and hygiene will become the top priority, even as contactless operations and automation will increase. Decentralization of operations to ensure business continuity will be a trend reversal from prominent consolidations over the past few years.

Retail Real Estate – In retail, online businesses will gain momentum – eCommerce giants have already added over 5,000 people to their delivery fleet during the lockdown period. Their consumer base expanded to senior citizens who have embraced technology in the COVID-19 era.

Mall revival will come with caveats. With hygiene and sanitation taking centre stage, malls which can offer these will benefit most in times to come.

Download the report ‘India Real Estate: A Different World Post COVID-19